The Barefoot Investor Buckets involve setting up your bank accounts into different ‘buckets’ as a way of reaching financial goals and building wealth. Read on as I explain more..

Introduction – Barefoot Investor Buckets

Most people across Australia have at least heard of Scott Pape’s brilliant book called The Barefoot Investor: The Only Money Guide You’ll Ever Need. By following the advice of this renowned financial expert, many people have found success in using his methods to manage their finances and grow wealth. It was literally the first personal finance book I read and honestly, I feel like it changed my relationship with money for the better. Scott’s approach to financial management is aimed at helping people build long-term wealth by structuring their spending to pay off debts, live frugally, plan for savings and achieve financial success.

A key component of the barefoot investor method involves the dividing of funds into a series of ‘buckets’ to help limit spending and prioritise the paying off of debts along the road to financial freedom. So, what are these ‘barefoot investor buckets’ and how do they work? Keep reading for a closer look at Scott Pape’s 3-bucket money management approach.

What are the Barefoot Investor Buckets?

Everyone dreams of a comfortable retirement. At its very heart, the purpose of the barefoot investor method is to reduce daily expenses to create a surplus that can be utilised to pay off debts and then grow net worth. For me, reducing expenses also involved boosting my surplus income. I think I took Scott Pape’s tips to the extreme and I began selling my clutter, as well as other people’s items too, making THOUSANDS in extra cash. You can read my article on exactly how I made so much, selling items online.

The barefoot investor system or ‘buckets’ are a way to structure your bank accounts to help achieve financial goals and create a secure future. Scott Pape suggests the use of three distinct buckets and these are outlined below.

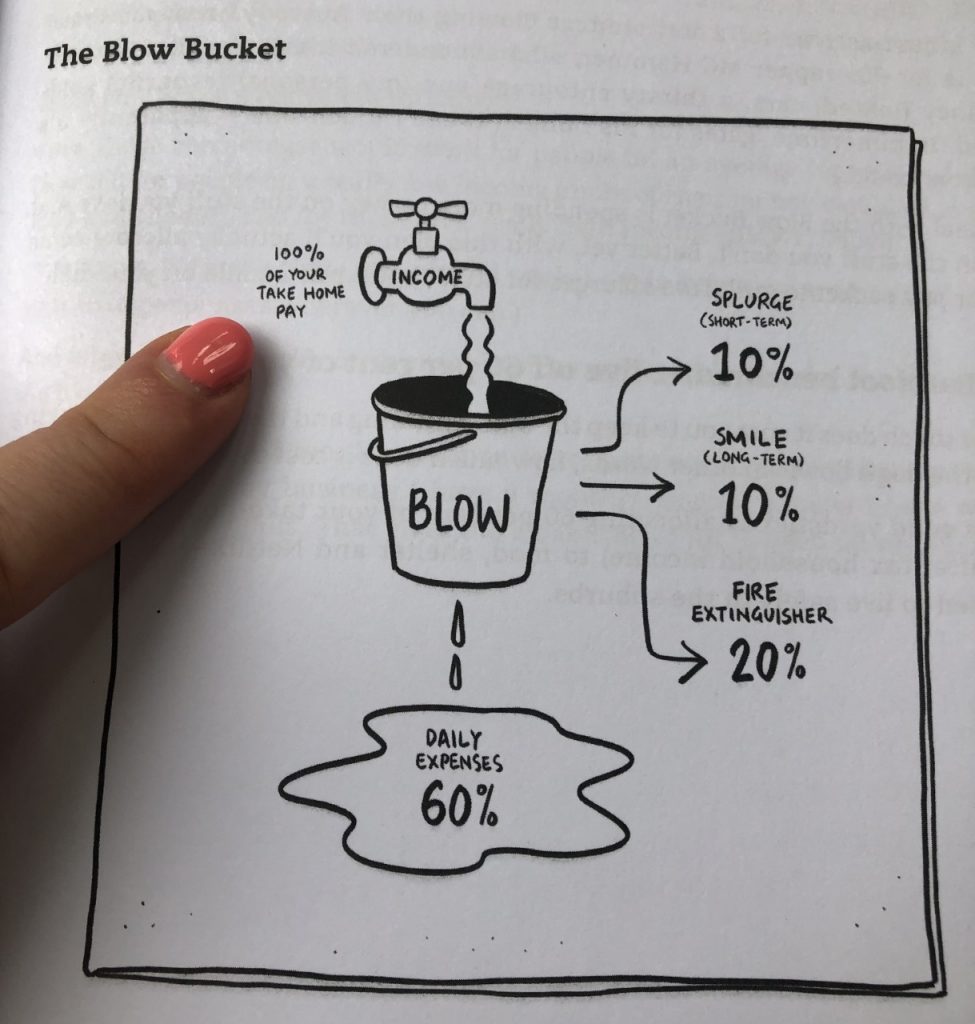

The ‘blow’ bucket

This bucket is also known as the ‘everyday bucket’ and is where all of your income will initially go. The blow bucket is for the day-to-day expenses that come with life. This bucket will cover the cost of food and regular bills and will also be used for recreation activities, the occasional splurge and big purchases such as holidays as it also includes a ‘splurge’ bank account. The blow bucket is basically the money that you will spend in the short term.

The ‘mojo’ bucket

This bucket is also known as the ‘emergency savings bucket’ and will replace the need for accruing further debt. The mojo bucket is used for emergencies, or to fight financial fires, and is a safety net for any unexpected financial expenses that might come up. This bucket will receive money from the blow bucket, and in time will overflow into the grow bucket.

The barefoot investor approach recommends starting with $2000 in this bucket and once debts are paid off, maintaining a minimum of three months living expenses as a decent-sized emergency fund. I have recently built my Emergency Fund to $24,000 and I’m so thankful I did, as it allowed me to feel secure enough to quit my toxic workplace! This mojo account can be kept in a mortgage offset, as mine is, or in a long term savings account, or any other account you deem appropriate.

The ‘grow’ bucket

This bucket is also known as the ‘investment bucket’ and is where you can build your long-term wealth and increase your net worth. Upon reaching your target amount within the ‘mojo’ bucket, the overflow will be placed into this ‘grow’ bucket (or smile account) to use for investment. These investments can include things like a super fund, long term savings accounts, shares, currencies or an investment property. However you decide to invest your funds from the ‘grow’ bucket is totally up to you. The important thing to remember here is that this money is for future you. It’s what will help to build your overall wealth, especially if you can take advantage of the magic of compound interest. : )

Scott Pape is a strong advocate for the orange ING cards for splitting up your ‘buckets’ into different ‘Barefoot Investor bank accounts’. Of course, there are many options for digital banks these days but personally, I do have an ING bank account, which is a separate account to my EF, and have been very happy with it. Other great alternatives are also Up bank and U bank.

It’s up to you how many cards you apply for but whichever bank you decide to use, keep an eye on bank fees, and you can usually order different cards for multiple bank accounts (or different ‘buckets’).

For more information about setting up your buckets, visit the Barefoot Investor website.

You can find Scott Pape’s book, The Barefoot Investor: The Only Money Guide You Will Ever Need, at most bookstores including Big W, Booktopia, Amazon and Dymocks.

How does Liz from TeachingBrave set up her Barefoot Investor buckets?

I have 100% of my pay going into my Mojo bucket – which is my Mortgage Offset account and also my safety money, or Emergency Fund. I am consumer debt free so I no longer have a need for a ‘Fire Extinguisher’ or fire extinguisher account (to put out emergency fires, also known as high-interest debt such as credit card debt, high-interest personal loans or car loans). Having my emergency fund in my offset account reduces the interest I’m paying on my home loan repayments which makes a big difference. I have now built this emergency fund bank balance to $24k.

My splurge bucket is also in my Mojo bucket. My daily expenses come out of my daily expenses account or my credit cards – as I have learned to use these responsibly. I usually top the credit cards up so they have more than the limit, and I always make sure I pay off the balance each month so I’m not paying any extra on interest. Using these cards often gives me extra FlyBuys points or other point rewards which I can redeem later for credit on groceries. I have a debit card linked to my offset account and I can use my Emergency fund as needed with this.

My Grow bucket consists of my Superannuation which I have in Hostplus and the shares I have purchased through Pearler. I do the easiest, laziest purchases of ETF’s including A200 shares, Vanguard VEU and VTS shares and just sit back and watch them grow! (and dip from time to time), but it’s been exciting to build my wealth in the way of shares and I’m happy I made the switch to Pearler as they have a lot of attractive features such as auto-invest, a super easy to use App, awesome customer service and template portfolios for inspiration!

Setting up your Barefoot buckets is very personal and will vary depending on your personal financial situation, as well as how you choose to manage your money. There are many options – Scott Pape simply makes suggestions on one way you could do it, but in reality, there are many ways you could set up your buckets.

What does the Barefoot Investor teach you?

The barefoot investor is all about building the confidence to effectively manage finances, pay off debts and ultimately build wealth. The book accounts for the different stages of life that people move through and gives a clear strategy for managing money without having to spend a lot of time budgeting.

Scott, in fact, is not a fan of budgeting at all due to the time investment and planning that is involved. Instead, his method will teach you how to spend less time worrying about money whilst simultaneously working towards your financial goals.

You can hear Scott Pape talking about his reasons behind his unique approach here: (608) Scott Pape the Barefoot Investor (Extended interview from Silic & Lee Show 1.6) – YouTube

What is the splurge account for?

Whilst the barefoot investor approach aims to help people be clever with money and build wealth, it also recognises the importance of living a fulfilling life. Scott encourages couples to take regular and planned ‘date nights’ and to engage in enjoyable activities and purchases that keep life joyful and fun.

Within the ‘blow’ bucket, Scott suggests keeping 10% of your income in a separate bank account which is your splurge account (guilt free spending money). This money is to spend on anything you want. It might be for purchases such as a nice pair of shoes or a new watch. It might be for going to the movies or buying coffee from your favourite barista. The splurge bank account will allow you to have money to spend on things that make you happy.

What are the Barefoot Investor steps?

The barefoot investor book will walk you through a total of 9 steps towards financial freedom. These steps are clear and simple and whilst I have listed them below, you can hear more about them in the following video clip: The Barefoot Investor: 9 steps to financial freedom | RBK Advisory

Step 1 – Schedule a monthly barefoot date night to have the conversations with your spouse that are needed to get the accounts set up and then to ensure that regular conversations occur in relation to financial matters.

Step 2 – Set up the buckets.

Step 3 – Domino your debts to help you get out and stay out of debt.

Step 4 – Buy your home.

Step 5 – Increase your superannuation to 15% to secure your future.

Step 6 – Boost your mojo to ensure 3 months of living expenses are available for emergencies.

Step 7 – Get the banker off your back. Pay off home loans as fast as you can. (Might be best to speak to a financial planner and/or a mortgage broker about this step).

Step 8 – Nail your retirement strategy.

Step 9 – Leave a legacy and think about how you want to be remembered.

Summary – Barefoot Investor Buckets

Thousands of people across the country have reported success in using the barefoot investor approach to financial management. Scott’s book, The Barefoot Investor for Families has proven just as popular as his first book and is helping the next generation learn how to thoughtfully control their spending and grow savings for a secure future.

After reading Barefoot for Families, I discussed a lot of the ideas and principles with my son Andy and he was more than enthusiastic, setting up jars (Save, Spend, Give) for himself! He now splits his pocket money between these jars, sometimes choosing to invest the money in his save jar, instead of leaving it sitting in there as cash.

As a previous victim of financial abuse, I strongly believe that it’s never too late to make changes to the way we manage our money and there is something in the barefoot investor approach for everyone. Don’t just take my word for it…check out the amazing reviews on Amazon.

You can read my Single Mum’s Money journey here. I am so thankful I turned my financial situation around. I’m no longer broke. I saved, I read books and listened to podcasts, learning about personal finance, I paid off all consumer debt, saved a house deposit and built my net worth, which has all set me up for a healthier financial future. Barefoot was a big part of that.

You can change your financial situation too. Or have you already? Tell me!

You might also be interested in my other money related articles as follows:

Single Parenting Payment: What Am I Entitled To?

Emergency Fund; Why, Where, and How Much?

Subsidy For Childcare; Everything You Need To Know

Do You Op Shop? 10 Reasons To Op Shop!

12 Ways To Get Free Food Or Free Groceries

Discaimer: None of this information is meant to be taken as personal financial advice. This is a basic review and my own personal experience. I am not a financial advisor and you should always do your own research when it comes to financial decisions and seek advice from a professional financial advisor who can guide you based on your own financial situation.

Thanks for sharing your thoughts on barefoot investor buckets. Very useful information for investors.

Thanks Joe! I’m glad it provided some real value for you.. Have you read the Barefoot Investor book?